Should You Sell Your Home Before Buying Another One?

Should You Sell Before Buying?

For many homeowners across Middle Tennessee, this is one of the biggest questions they'll face.

Should you sell your current home first?

Or should you buy your next home before listing your existing one?

Unfortunately, there isn't a universal answer.

The right strategy depends on your finances, your risk tolerance, your timeline, the current housing market, and the type of home you're trying to buy.

In neighborhoods across Nashville, Franklin, Brentwood, Hendersonville, Gallatin, Mount Juliet, Lebanon, and surrounding communities, homeowners ask this question every week.

Some are moving because they need more space.

Others are downsizing after retirement.

Many are relocating for work.

Some are upgrading into luxury homes.

Others simply want a different neighborhood.

Every situation is different.

The good news?

With proper planning, you can dramatically reduce stress, avoid expensive mistakes, and create a smooth transition from one home to the next.

This guide will walk you through every major consideration so you can make the decision that's best for your family.

Nashville's Nik

Nik Shewmaker | REALTOR® | Real Broker

📞 (615) 585-0022

Key Takeaways

- There is no one-size-fits-all answer.

- Selling first offers more financial certainty.

- Buying first provides convenience but increases financial risk.

- Your local market conditions matter more than national headlines.

- Careful planning can eliminate many common moving headaches.

- Several financing options can help homeowners buy before selling.

- Working with an experienced REALTOR® helps coordinate both transactions successfully.

Why Timing Matters More Than Ever

Buying and selling at the same time can feel like trying to solve two puzzles simultaneously.

Questions quickly begin piling up.

- What if your current home doesn't sell?

- What if it sells too quickly?

- What if your dream home appears before you're ready?

- What if interest rates change?

- What if home prices rise while you're waiting?

These concerns are completely normal.

The encouraging news is that nearly every one of these situations has a solution when you prepare ahead of time.

Instead of hoping everything works out, successful homeowners create a plan before they ever list their home.

That plan starts with understanding today's market.

Understanding Today's Nashville Housing Market

Every housing market has its own rhythm.

Middle Tennessee continues to attract buyers from across the country because of:

- Strong employment opportunities

- No state income tax

- Diverse economy

- Quality healthcare

- Excellent universities

- Outdoor recreation

- Music, entertainment, and culture

While the market has become more balanced compared to the frenzy of recent years, desirable homes that are priced correctly still receive significant attention.

However, buyers today are more selective.

They're comparing homes carefully.

They're negotiating more often.

Inspection requests have become more common.

Pricing strategy matters more than ever.

This balanced environment means timing both your purchase and your sale requires thoughtful planning rather than guesswork.

Whether you're moving within Nashville or relocating to Brentwood, Franklin, Hendersonville, Gallatin, Mount Juliet, Lebanon, or another Middle Tennessee community, understanding your local market conditions is one of the most important factors in creating a successful buying and selling strategy.

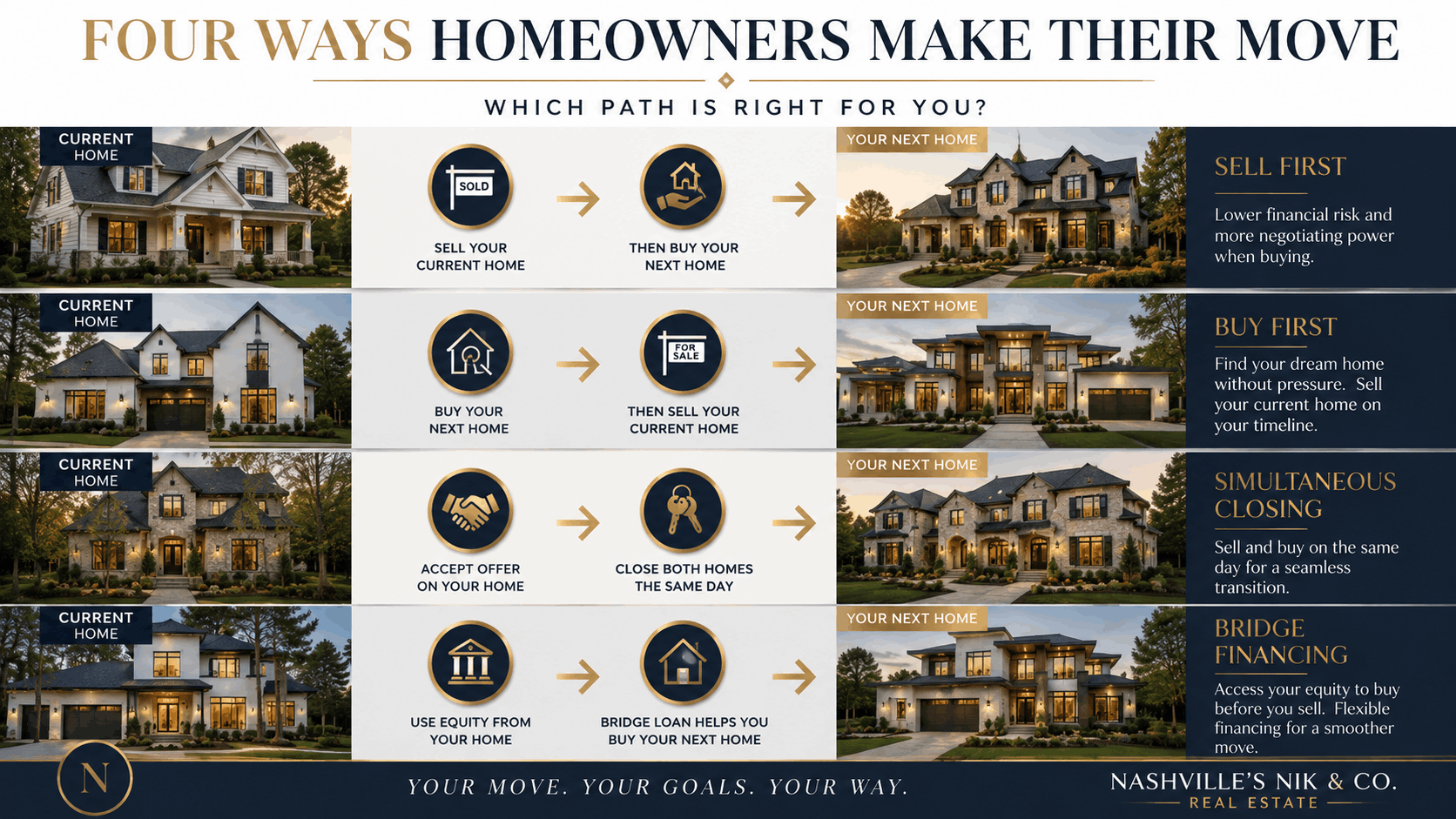

The Four Common Moving Scenarios

Most homeowners fall into one of four categories.

Understanding which describes your situation is the first step.

Scenario 1: Sell First, Then Buy

This is the most conservative financial approach.

You sell your home.

Know exactly how much money you'll have available.

Then shop for your next property.

Advantages

- No double mortgage payments

- Strong understanding of your budget

- Lower financial risk

- Easier loan approval

- Greater negotiating confidence

Potential Downsides

- Temporary housing may be necessary.

- Multiple moves may be required.

- You may feel pressure to find a replacement quickly.

Scenario 2: Buy First, Then Sell

Some homeowners purchase their next home before listing their current property.

This allows for a smoother transition.

You move once.

You aren't rushing to pack immediately after closing.

You can prepare your current home while already living elsewhere.

Advantages

- Less stress during moving

- Easier home preparation

- Better staging opportunities

- More flexibility

Potential Downsides

- Carrying two mortgages

- Higher financial exposure

- Qualifying for two homes

- Increased monthly expenses

Scenario 3: Buy and Sell Simultaneously

This is one of the most common approaches.

The goal is coordinating both closings within days—or even hours—of one another.

When everything aligns, it feels seamless.

However, coordinating inspections, appraisals, financing, title work, moving trucks, utilities, and possession dates requires detailed planning.

A knowledgeable REALTOR® becomes invaluable during this process.

Scenario 4: Use Alternative Financing

Today's homeowners have more financing solutions available than ever before.

Depending on your financial situation, options may include:

- Bridge loans

- Home equity lines of credit (HELOCs)

- Home equity loans

- Cash-backed purchase programs

- Buy-before-you-sell financing

- Delayed financing strategies

Each option has advantages and potential drawbacks.

Choosing the right one depends on your financial goals and overall risk tolerance.

The Biggest Financial Questions to Ask Yourself

Before deciding on any strategy, ask yourself several important questions.

Can You Comfortably Afford Two Mortgage Payments?

Even if only for a few months?

Many homeowners underestimate how quickly expenses add up.

You may temporarily pay for:

- Two mortgage payments

- Two utility bills

- Two insurance policies

- Lawn maintenance

- Property taxes

- HOA dues

- Unexpected repairs

If this creates financial stress, selling first may provide greater peace of mind.

How Much Equity Do You Have?

Equity often determines your flexibility.

For example:

If your home sells for $700,000 and you owe $300,000, you have approximately $400,000 in equity before closing costs.

That equity may become your next:

- Down payment

- Emergency reserve

- Remodeling budget

- Investment opportunity

Knowing this number early helps determine which strategy makes the most sense.

Are You Comfortable With Risk?

Every homeowner has a different comfort level.

Some prefer certainty.

Others value convenience.

Neither is right or wrong.

The important thing is choosing a strategy that allows you to sleep well at night.

Financial peace of mind often outweighs attempting to perfectly time the market.

Market Conditions Can Change Your Strategy

The local housing market significantly influences which approach works best.

In a Strong Seller's Market

Homes sell quickly.

Inventory is limited.

Buyers compete aggressively.

Selling first may feel less risky because your home is likely to attract interest quickly.

However, purchasing your replacement home may become more competitive.

In a Balanced Market

Today's Nashville-area market resembles this in many neighborhoods.

Homes still sell.

Buyers have more choices.

Negotiations become more common.

Pricing becomes increasingly important.

In balanced conditions, careful planning becomes more valuable than speed.

In a Buyer's Market

If inventory rises substantially:

Homes may take longer to sell.

Buyers gain negotiating power.

Selling first could require additional patience.

Buying opportunities may improve.

Understanding these cycles helps homeowners make smarter long-term decisions instead of reacting emotionally.

The Emotional Side of Moving

Buying and selling isn't purely financial.

It's emotional.

You're leaving a place filled with memories.

You're making one of the largest financial decisions of your life.

It's perfectly normal to feel:

- Excited

- Nervous

- Overwhelmed

- Hopeful

- Uncertain

The key is separating emotion from strategy.

A well-planned move reduces stress because you're making informed decisions rather than emotional ones.

Financing Options That Can Make Moving Easier

One of the biggest misconceptions homeowners have is believing they only have two choices:

- Sell first.

- Buy first.

In reality, there are several financing strategies that can make moving much smoother.

Not every option is right for every homeowner, but understanding what's available allows you to choose the strategy that best fits your situation.

Bridge Loans

A bridge loan is exactly what it sounds like.

It "bridges" the financial gap between selling your current home and purchasing your next one.

Instead of waiting for your existing home to close, a lender provides short-term financing based on the equity you've already built.

Once your current home sells, the bridge loan is typically paid off.

When a Bridge Loan Can Make Sense

Bridge financing may be worth exploring if:

- You've found your dream home.

- You have substantial equity.

- You're confident your current home will sell.

- You want to avoid moving twice.

Advantages

- Purchase before selling.

- Greater flexibility.

- Less pressure.

- Only one move.

Things to Consider

Bridge loans often carry:

- Higher interest rates than traditional mortgages.

- Short repayment periods.

- Additional closing costs.

- Qualification requirements.

For some homeowners, the convenience outweighs these added costs. For others, selling first remains the better financial decision.

Home Equity Lines of Credit (HELOCs)

If you've owned your home for several years, you may have built significant equity.

A Home Equity Line of Credit, commonly called a HELOC, allows you to borrow against a portion of that equity before selling.

Many homeowners use these funds for:

- Down payments

- Earnest money

- Moving expenses

- Minor renovations on the current home

- Temporary cash flow needs

Unlike a bridge loan, a HELOC often provides more flexibility because you only borrow what you actually use.

However, qualification depends on your income, credit, available equity, and lender guidelines.

Home Equity Loans

A home equity loan differs slightly from a HELOC.

Instead of a revolving line of credit, you receive one lump sum with fixed repayment terms.

This option may appeal to homeowners who know exactly how much they'll need before selling.

Buy-Before-You-Sell Programs

Over the past several years, new financing programs have become increasingly popular.

Some lenders and companies now offer programs specifically designed for homeowners who want to purchase before selling.

While each program works differently, many allow homeowners to:

- Buy their replacement home first.

- Move at their own pace.

- Prepare the previous home for sale after moving.

- Sell without the stress of showing a lived-in home.

These programs aren't available to everyone, but they're worth discussing with your lender if convenience is your highest priority.

Should You Make a Contingent Offer?

Another common strategy involves writing an offer that is contingent upon selling your current home.

Simply put, you're telling the seller:

"I'll buy your home after mine successfully sells."

Benefits

- Lower financial risk.

- No need for two mortgages.

- No bridge financing required.

Drawbacks

In competitive markets, sellers often prefer offers without contingencies.

If several buyers are interested, a contingent offer may lose to someone who's already sold their home or is paying cash.

That doesn't mean contingent offers never work.

It simply means your overall offer needs to be as attractive as possible.

Rent-Back Agreements

One of the easiest ways to reduce moving stress is negotiating a rent-back agreement.

Here's how it works.

You sell your home.

You close.

Instead of moving immediately, you remain in the property for an agreed-upon period while paying rent—or sometimes no rent at all, depending on negotiations.

This gives you additional time to:

- Close on your next home.

- Finish renovations.

- Coordinate movers.

- Avoid temporary housing.

Many homeowners don't realize this option exists.

When negotiated properly, it can dramatically simplify the transition.

How to Coordinate Two Closings

The goal for many homeowners is making everything happen almost simultaneously.

While every transaction is different, here's a common timeline.

- List your current home.

- Accept an offer.

- Begin shopping seriously for your replacement home.

- Negotiate possession dates.

- Schedule inspections.

- Coordinate financing.

- Finalize moving plans.

- Close on both homes within a few days—or sometimes even the same day.

- While this sounds simple, dozens of moving pieces must stay aligned.

- That's why communication between your REALTOR®, lender, title company, inspectors, and movers becomes incredibly important.

Should You Prepare Your Home Before Shopping?

One mistake homeowners often make is waiting until they've found another home before preparing their current one.

Instead, begin preparing early.

You don't necessarily need to list immediately.

But you should begin:

- Decluttering.

- Deep cleaning.

- Completing repairs.

- Organizing storage.

- Painting if needed.

- Improving curb appeal.

By the time you're ready to list, your home can hit the market quickly if the perfect replacement property appears.

Preparation creates flexibility.

The Hidden Costs Homeowners Forget

Moving involves much more than commissions and mortgage payments.

Many homeowners overlook expenses such as:

- Professional movers

- Packing supplies

- Utility connection fees

- Storage units

- Temporary housing

- Cleaning services

- Lawn maintenance

- Minor repairs

- Appliance replacements

- Window treatments

- Furniture purchases

Creating a detailed moving budget early helps eliminate surprises later.

Common Mistakes to Avoid

Even experienced homeowners occasionally make avoidable mistakes.

Waiting Too Long to Meet With a REALTOR®

Many people begin browsing homes months before understanding what their own home is worth.

Knowing your home's market value should come first.

Assuming Online Estimates Are Accurate

Automated valuation tools can provide a rough estimate.

They cannot:

- Evaluate updates.

- Understand neighborhood trends.

- Measure condition.

- Compare unique floor plans.

- Account for premium lots.

A professional pricing analysis provides far greater accuracy.

Falling in Love Too Early

It's easy to emotionally commit to a home before knowing whether your current property will sell.

Keeping emotions balanced until both transactions are progressing reduces disappointment.

Overpricing Your Current Home

Trying to "leave room for negotiation" often backfires.

Today's buyers are well-informed.

Homes priced correctly typically receive more attention, stronger offers, and often sell faster than overpriced homes requiring repeated price reductions.

Ignoring the Local Market

National headlines don't always reflect what's happening in Middle Tennessee.

Every community has its own inventory levels, buyer demand, and pricing trends.

A strategy that works in one city may not be ideal just a few miles away.

Special Considerations for Different Homeowners

Growing Families

If you're moving because you've outgrown your current home, school calendars and minimizing disruption for children may influence your timing.

Summer often provides additional flexibility.

Empty Nesters

Many homeowners downsizing have accumulated decades of belongings.

Allow extra time for:

- Donating.

- Selling furniture.

- Estate planning.

- Organizing keepsakes.

The emotional side of moving is often greater than expected.

Luxury Homeowners

Higher-end properties sometimes require longer marketing periods because the buyer pool is naturally smaller.

Planning ahead becomes even more important when selling luxury real estate.

Relocating Professionals

If you're moving because of a job transfer, timing may be dictated by employment start dates.

Building extra flexibility into your plan helps reduce last-minute stress.

How Today's Nashville Market Impacts Your Decision

One of the biggest mistakes homeowners make is relying on national real estate headlines to make local decisions.

While national trends provide context, real estate has always been local.

A home in Green Hills behaves differently than one in Gallatin.

A waterfront property on Old Hickory Lake has different buyer demand than a townhome in East Nashville.

Luxury homes in Brentwood often have different timelines than starter homes in Hendersonville.

That's why your moving strategy should be based on your neighborhood, your price range, and your goals, not just what you hear on the news.

An experienced local REALTOR® can help you answer questions like:

- How quickly are homes like mine selling?

- How many competing listings are on the market?

- What concessions are buyers asking for?

- Is inventory increasing or decreasing?

- Will my home likely receive multiple offers?

- Is this a good time to upgrade, downsize, or relocate?

Understanding these local factors often determines whether selling first or buying first is the smarter decision.

Sample Timeline: Selling Before Buying

Here's what a well-organized move might look like if you choose to sell first.

Weeks 1–2

- Meet with your REALTOR®.

- Receive a comparative market analysis.

- Discuss pricing strategy.

- Create a moving plan.

Weeks 2–4

- Complete repairs.

- Declutter.

- Stage the home.

- Schedule professional photography, video, drone footage, and floor plans.

Week 5

- List your home.

- Launch marketing.

- Begin showings.

Weeks 6–8

- Accept an offer.

- Negotiate inspections.

- Finalize your next-home budget.

- Begin actively shopping.

Weeks 8–12

- Go under contract on your next home.

- Coordinate financing.

- Schedule movers.

- Transfer utilities.

Closing Week

- Close on your current home.

- Purchase your new home.

- Move once if the timelines align—or use a negotiated rent-back if needed.

Sample Timeline: Buying Before Selling

If you decide to purchase first, your timeline may look a little different.

- Meet with a lender.

- Understand exactly what you qualify for.

- Discuss bridge financing, a HELOC, or other buy-before-you-sell options if needed.

- Begin shopping for your next home.

- Go under contract.

- Move into your new home.

- Prepare your previous home.

- List and sell after you've already moved.

This approach often creates a more relaxed moving experience, but it also requires careful financial planning.

Questions Every Homeowner Should Ask

Before deciding on a strategy, consider these questions.

Do I know my home's current market value?

Many homeowners are surprised by how much equity they've built.

A current market analysis provides a much clearer picture than an online estimate.

Could I qualify for another mortgage?

Even if you have significant equity, your lender will evaluate:

- Income

- Debt-to-income ratio

- Credit history

- Existing obligations

- Cash reserves

Understanding this before shopping helps prevent disappointment.

What happens if my home takes longer to sell?

A good plan should include backup options.

For example:

- Price adjustments

- Extended closing dates

- Temporary financing

- Rent-back agreements

- Bridge financing

Preparing for different outcomes reduces stress if the unexpected happens.

What if I receive multiple offers?

Receiving multiple offers doesn't automatically mean accepting the highest price.

Other factors may include:

- Financing strength

- Inspection contingencies

- Appraisal gaps

- Closing timelines

- Possession dates

Sometimes the strongest overall offer isn't the highest-dollar offer.

The Importance of a Customized Strategy

No two homeowners have the same priorities.

You may value certainty.

Someone else values convenience.

Another homeowner wants to maximize every dollar of equity.

Someone relocating for work may simply need speed.

That's why the best approach isn't a generic checklist.

It's a personalized strategy based on your goals, finances, timeline, and lifestyle.

How I Help Homeowners Navigate Both Transactions

Buying and selling at the same time can feel overwhelming.

My role is to simplify the process.

When working together, we'll create a plan that coordinates every major milestone, including:

- Determining your home's current market value.

- Reviewing neighborhood market conditions.

- Building a personalized timeline.

- Coordinating with your lender.

- Identifying financing options when appropriate.

- Preparing your home for maximum buyer appeal.

- Developing a pricing strategy.

- Scheduling photography, video, drone footage, and floor plans.

- Marketing your home professionally.

- Negotiating offers.

- Coordinating inspections, appraisals, title work, and closing.

- Helping you search for your next home at the right time.

The goal isn't simply to buy or sell a house.

It's to make your move as smooth, organized, and financially sound as possible.

Key Takeaways

- Every homeowner's situation is unique.

- Selling first provides financial certainty and minimizes risk.

- Buying first offers convenience but often requires additional financial planning.

- Bridge loans, HELOCs, rent-back agreements, and buy-before-you-sell programs can provide flexibility.

- Market conditions in your specific Nashville-area neighborhood matter more than national headlines.

- Preparing your current home before shopping for the next one gives you more options.

- Working with an experienced REALTOR® can help coordinate both transactions and reduce stress.

Nik's Pro Tip

Many homeowners start looking at homes online before knowing what their current home is actually worth. I recommend beginning with a professional home value consultation. Understanding your home's current value, available equity, and today's local market gives you the confidence to make smart decisions and helps eliminate surprises during the buying and selling process.

Call to Action

If you're thinking about making a move, don't wait until you've found your next home to start planning.

A conversation today can help you understand:

- What your current home is worth.

- How much equity you may have.

- Which moving strategy best fits your goals.

- What today's local market means for your timeline.

- How to avoid common mistakes that can cost time and money.

Whether you're upsizing, downsizing, relocating, or simply exploring your options, having a personalized plan can make all the difference.

Related Seller Resources

✓ How Much Is My Nashville Home Worth?

✓ The True Cost of Selling a Home in Nashville

✓ The Complete Nashville Home Selling Timeline

✓ When Is the Best Time to Sell a Home in Nashville?

✓ How to Price Your Home to Sell for Top Dollar

✓ 27 Things Every Nashville Homeowner Should Do Before Listing Their Home

✓ Pre-Listing Repairs That Add Value

✓ 11 Costly Mistakes Nashville Homeowners Make When Selling Their Home

✓ How to Sell Your Nashville Home for the Highest Possible Price

✓ Best Realtor in Nashville: How to Choose the Right Listing Agent

✓ Downsizing Your Home in Nashville

✓ Thinking About Selling Your Nashville Home? Here's Why Hundreds of Homeowners Choose Nashville's Nik

Contact Nashville's Nik

Whether you're moving across town or across Middle Tennessee, I'd be honored to help you create a strategy that fits your goals and makes the transition as smooth as possible.

I proudly help homeowners throughout Nashville, Brentwood, Franklin, Hendersonville, Gallatin, Mount Juliet, Lebanon, College Grove, White House, Green Hills, Forest Hills, Old Hickory Lake, and surrounding communities.

Nashville's Nik

Nik Shewmaker | REALTOR® | Real Broker

📞 (615) 585-0022

If you're wondering whether you should sell before buying—or buy before selling—I'd be happy to walk you through your options, answer your questions, and build a customized plan designed around your timeline and financial goals.

FAQs

1. Should I sell my house before buying another one?

It depends on your financial situation, available equity, and comfort with risk. Selling first gives you a clear budget and avoids carrying two mortgages, while buying first can make moving easier if you qualify for financing.

2. Is it better to buy a home before selling my current one in Nashville?

In some cases, yes. If you have substantial equity, strong income, or qualify for a bridge loan or buy-before-you-sell program, purchasing first may provide more flexibility. However, it's important to understand the financial risks before choosing this approach.

3. What is a bridge loan, and how does it work?

A bridge loan is a short-term loan that allows homeowners to use the equity in their current home to purchase another home before their existing property sells. Once the original home sells, the bridge loan is typically paid off.

4. Can I make an offer on a new home before my current home sells?

Yes. Many buyers submit offers that are contingent upon the sale of their current home. While this can reduce financial risk, contingent offers may be less competitive in a fast-moving market.

5. What is a rent-back agreement?

A rent-back agreement allows you to sell your home but remain in it for an agreed-upon period after closing. This gives you additional time to purchase your next home and move without rushing.

6. How much equity do I need before buying another home?

There's no universal amount, but having significant equity can help fund your down payment, closing costs, and moving expenses. A REALTOR® and lender can help determine how much equity is available to you.

7. What are the risks of buying before selling?

The biggest risks include carrying two mortgage payments, higher monthly expenses, qualifying for additional financing, and your current home taking longer than expected to sell.

8. How do I know how much my current home is worth?

The most accurate way is through a Comparative Market Analysis (CMA) prepared by a local REALTOR®. Online home value estimates can be helpful, but they don't account for your home's condition, upgrades, or neighborhood trends.

9. How long does it usually take to buy and sell a home at the same time?

Every transaction is different, but many homeowners complete both transactions within 30 to 60 days. Careful planning and coordination between your REALTOR®, lender, and title company can help keep everything on schedule.

10. Should I prepare my home before I start shopping for another one?

Yes. Decluttering, making repairs, improving curb appeal, and completing professional staging before you begin shopping gives you more flexibility if the perfect home becomes available.

11. How does the Nashville housing market affect whether I should sell first or buy first?

Local inventory levels, buyer demand, interest rates, and your neighborhood's market conditions all play a role. A strategy that works in one part of Middle Tennessee may not be the best approach in another.

12. What financing options are available if I want to buy before selling?

Depending on your financial situation, options may include bridge loans, home equity lines of credit (HELOCs), home equity loans, buy-before-you-sell programs, or other specialized financing solutions offered by lenders.

13. What expenses should I budget for when moving?

In addition to your mortgage and closing costs, remember to budget for movers, packing supplies, utility transfers, storage, cleaning services, repairs, insurance, and any temporary housing expenses if needed.

14. Is it possible to move only once when buying and selling?

Yes. With proper planning, coordinated closing dates, or a negotiated rent-back agreement, many homeowners successfully move directly from their old home into their new one without needing temporary housing.

15. How can a REALTOR® help coordinate buying and selling at the same time?

A REALTOR® can help determine your home's value, develop a pricing strategy, coordinate timelines, negotiate contracts, communicate with your lender and title company, manage inspections and appraisals, and help ensure both transactions stay on track for a smoother move.

Categories

- All Blogs (277)

- -Brentwood--TN-vs--Franklin--TN---Which-Is-Better-for-You--Nashville-s-Nik-Compares-the-Two (1)

- -Does-It-Snow-in-Brentwood--TN--What-to-Expect-in-Every-Season---with-Nashville-s-Nik (1)

- -How-Far-Is-Brentwood--TN-from-Nashville--Nashville-s-Nik-Explains-the-Commute (1)

- -How-Far-Is-Brentwood--TN-from-Nashville--What-Locals-Really-Say---with-Nashville-s-Nik (1)

- -Is-Brentwood--TN-a-Good-Place-to-Invest-in-Real-Estate--Nashville-s-Nik-Shares-Market-Insights (1)

- -Is-Brentwood--TN-a-Good-Place-to-Live--Nashville-s-Nik-Explains-Why-Everyone-Loves-It (1)

- -Is-Brentwood--TN-a-Good-Place-to-Raise-a-Family--Nashville-s-Nik-Shares-What-Parents-Love-Most (1)

- -Is-Brentwood--TN-a-Good-Place-to-Retire--Nashville-s-Nik-Shares-the-Real-Story (1)

- -Is-Brentwood--TN-a-Good-Place-to-Retire--Nashville-s-Nik-Weighs-the-Pros-and-Cons (1)

- -Is-Brentwood--TN-a-Safe-Place-to-Live--Nashville-s-Nik-Breaks-Down-the-Facts (1)

- -Is-Brentwood--TN-a-Suburb-of-Nashville--Nashville-s-Nik-Explains-the-Connection (1)

- -Is-Brentwood--TN-Safe--What-You-Should-Know-Before-Moving---with-Nashville-s-Nik (1)

- -Moving-to-Brentwood--TN--Nashville-s-Nik-s-Complete-Relocation-Guide-for-2025 (1)

- -Top-5-Nashville-Suburbs-for-Out-of-State-Buyers (1)

- -What-Amenities-and-Parks-Does-Brentwood--TN-Offer--Nik-Shewmaker-s-Local-Favorites (1)

- -What-Are-the-Best-Neighborhoods-in-Brentwood--TN--Nashville-s-Nik-Shares-Local-Favorites (2)

- -What-Is-It-Like-Living-in-Brentwood--TN--A-Day-in-the-Life-with-Nashville-s-Nik (1)

- -What-Is-the-Cost-of-Living-in-Brentwood--TN--Nashville-s-Nik-Breaks-Down-Real-Numbers (1)

- -What-Is-the-Cost-of-Living-in-Brentwood--TN--Nashville-s-Nik-Explains-What-to-Expect (1)

- -What-Is-the-Cost-of-Living-in-Brentwood--TN--Nashville-s-Nik-Explains-What-to-Expect-in-2025 (1)

- -What-Jobs-Are-in-Brentwood--TN--Nashville-s-Nik-Breaks-Down-the-Local-Economy (1)

- -Why-Are-So-Many-People-Moving-to-Brentwood--TN--Nashville-s-Nik-Breaks-Down-the-Trend (1)

- -Why-Are-So-Many-People-Moving-to-Brentwood--TN--Nashville-s-Nik-Explains-the-Hype (1)

- 10 Things You Need to Know Before Moving to Nashville, Tennessee (1)

- 10-Mistakes-to-Avoid-When-Buying-a-Home-in-Nashville (1)

- 7 Steps Every First-Time Homebuyer in Tennessee Needs to Know (1)

- A Local’s Guide to the Best Coffee Shops in Middle Tennessee (1)

- best Realtor in Middle Tennessee (1)

- Best Realtor in Middle Tennessee: 9 Questions to Ask Before You Hire a Buyer’s Agent in 2025 (1)

- Best-Nashville-Neighborhoods-for-First-Time-Buyers-in-2025 (1)

- BEST-REALTOR-IN-MIDDLE-TENNESSEE--11-QUESTIONS-TO-ASK-BEFORE-YOU-HIRE-YOUR-AGENT-IN-2025 (1)

- Best-Realtor-in-Nashville---Franklin--7-Questions-to-Ask-Before-You-Hire-an-Agent-in-Middle-Tennessee (1)

- Best-Realtor-in-Nashville---Franklin--What-to-Ask-Before-Hiring-a-Middle-Tennessee-Real-Estate-Agent (1)

- Brentwood (1)

- Can I Sell My Home While in Forbearance in Nashville? (1)

- Can I Sell My Nashville Home Without a Realtor? (1)

- Can-I-Buy-My-First-Home-in-Nashville-With-Zero-Down- (2)

- Choosing-the-Right-Realtor-in-Middle-Tennessee--How-to-Hire-the-Best-Agent-in-2025 (1)

- Choosing-the-Right-Realtor-in-Middle-Tennessee--What-to-Ask-Before-You-Hire-in-2025 (1)

- Do-I-Really-Need-a-Buyer-s-Agent-When-Purchasing-in-Nashville- (1)

- Do-I-Really-Need-a-Buyers-Agent-When-Purchasing-in-Nashville (1)

- First-Time Buyers (1)

- First-Time Home Buyer in Nashville? Here’s What You Need to Know Before You Start (1)

- First-Time-Home-Buyer-in-Nashville (1)

- franklin (1)

- Hendersonville (1)

- Hendersonville Real Estate (1)

- Here are five top events happening in Nashville, Tennessee, in June 2025 (1)

- Hidden Gems: Unique Places to Visit in Middle Tennessee (1)

- Home Buying Tips (2)

- Home Preparation (1)

- Home Selling Tips (8)

- Home Values (2)

- How Do I Handle a Low Appraisal When Selling My Home in Nashville? (1)

- How Do I Know If I’m Ready to Sell My Home in Nashville? (1)

- How Do I Sell My Home Fast in Nashville? NashvillesNik’s Proven Plan (1)

- How Do I Sell My Home Quickly in Nashville, TN? (1)

- How Does Nashville’s Healthcare System Compare for Newcomers? (1)

- How Is the Real Estate Market in Brentwood, TN? Nashville’s Nik Gives the 2025 Update (1)

- How Long Does It Take to Sell a Home in Nashville, TN? (1)

- How Much Do I Really Need for a Down Payment on a Nashville Home? (1)

- How Much Does It Cost to Sell a Home in Brentwood, TN (1)

- How Much Does It Cost to Sell a Home in Nashville, TN? (2)

- How to Avoid Common Mistakes When Selling Your Home in Nashville, TN (1)

- How to Choose the Right Neighborhood in Middle Tennessee (1)

- How to Improve Your Credit Score Before Buying a Home in Nashville (1)

- How to Maximize Your Profit When You Sell Your Home in Nashville, TN (1)

- How to Sell a Home in a Changing Nashville Real Estate Market (1)

- How to Sell a Home in Nashville Without a Realtor (1)

- How to Sell a Home That Needs Repairs in Nashville, TN (1)

- How to Sell a Home With Solar Panels in Nashville (1)

- How to Sell Your Home As-Is in Mount Juliet, TN (1)

- How to Sell Your Home by Owner in Brentwood, TN (1)

- How to Sell Your Home Fast in Hendersonville, TN (1)

- How to Sell Your Home in Arlington, TN (1)

- How to Sell Your Home in Forest Hills, TN: A Smart Seller’s Guide (1)

- How to Sell Your Home in Nashville After a Divorce (1)

- How to Sell Your Home in Nolensville, TN: A Complete Guide (1)

- How to Sell Your Home in Oak Hill, TN: A Step-by-Step Guide (1)

- How to Sell Your Home in Spring Hill, TN: A Complete Guide (1)

- How to Sell Your Home Without Using a Realtor in Nashville, TN (1)

- How to Stage a Home for Sale in Nashville, TN (1)

- How-Are-the-Schools-in-Brentwood--TN--Nik-s-Expert-Overview (1)

- How-Do-I-Buy-a-Home-in-Nashville--TN (1)

- How-Do-Nashville-s-Commute-Times-Compare-for-Relocators- (1)

- How-Do-Nashville-s-Grocery-and-Shopping-Options-Compare-for-Newcomers- (1)

- How-Do-Nashville-s-Job-Opportunities-Compare-for-Relocators- (1)

- How-Do-Nashville-s-Neighborhoods-Differ-for-New-Residents- (1)

- How-Do-Nashville-s-Parks-and-Outdoor-Spaces-Compare-for-Families- (1)

- How-Do-Nashville-s-Schools-Rank-for-Families-Moving-Here- (1)

- How-Do-Nashville-s-Taxes-Compare-for-New-Residents- (1)

- How-Do-Nashville-s-Utilities-and-Internet-Compare-for-New-Residents- (1)

- How-Does-Brentwood--TN-Compare-to-Franklin--Nashville-s-Nik-Breaks-Down-the-Differences (1)

- How-Does-Nashville-s-Cost-of-Living-Compare-to-Other-U-S--Cities- (1)

- How-Does-Nashville-s-Food-Scene-Compare-for-New-Residents- (1)

- How-Does-Nashville-s-Housing-Market-Compare-for-Relocators- (1)

- How-Does-Nashville-s-Housing-Market-Compare-to-Other-Cities- (1)

- How-Does-Nashville-s-Public-Transit-Compare-for-Newcomers- (1)

- How-Does-Nashville-s-School-System-Compare-for-Relocating-Families- (1)

- How-Does-Nashville-s-Weather-Compare-for-Relocators- (1)

- How-Far-Is-Brentwood--TN-from-Franklin--Nashville-s-Nik-Explains-the-Local-Connection (1)

- How-Far-Is-Brentwood--TN-from-Nashville--Nashville-s-Nik-Explains-the-Commute--Traffic--and-Access (1)

- How-Interest-Rate-Changes-Could-Impact-Your-Nashville-Home-Purchase (1)

- How-Is-Nashville-s-Commute-and-Public-Transportation-for-Newcomers- (1)

- How-Long-Does-It-Take-to-Buy-a-Home-in-Nashville--TN- (1)

- How-Much-Do-I-Really-Need-for-a-Down-Payment-on-a-Nashville-Home- (1)

- How-Much-Does-It-Cost-to-Live-in-Brentwood--Tennessee--Nik-Shewmaker-Explains (1)

- How-Much-Does-It-Really-Cost-to-Relocate-to-Nashville- (1)

- How-Much-House-Can-I-Afford-in-Nashville- (1)

- How-Nashville-s-Growth-Is-Affecting-First-Time-Home-Buyers (1)

- How-to-Avoid-Buyer-s-Remorse-When-Purchasing-a-Home-in-Nashville (1)

- How-to-Avoid-Overpaying-for-a-Home-in-Nashville-s-Popular-Areas (1)

- How-to-Buy-a-Condo-in-Nashville---What-You-Need-to-Know (1)

- How-to-Buy-a-Fixer-Upper-in-Nashville-Without-Breaking-the-Bank (1)

- How-to-Buy-a-Home-in-Nashville-on-a-Tight-Budget---Real-Strategies-That-Work (1)

- How-to-Buy-a-Home-in-Nashville-When-You-re-Relocating-From-Another-State (1)

- How-to-Buy-a-Home-in-Nashville-with-Bad-Credit (1)

- How-to-Buy-a-Home-in-Nashville-Without-Regretting-It-Later (1)

- How-to-Buy-a-Home-in-Nashville-Without-Selling-Your-Current-House-First (1)

- How-to-Buy-a-Home-in-Tennessee-When-You-Live-Out-of-State (1)

- How-to-Buy-Your-First-Home-in-East-Nashville-Without-Getting-Overwhelmed (1)

- How-to-Choose-the-Best-Listing-Agent-in-Middle-Tennessee (1)

- How-to-Choose-the-Best-Listing-Agent-in-Middle-Tennessee-to-Sell-Your-Home (1)

- HOW-TO-CHOOSE-THE-BEST-LISTING-AGENT-IN-MIDDLE-TENNESSEE-TO-SELL-YOUR-HOME-FAST (1)

- How-to-Choose-the-Best-Realtor-in-Brentwood--Tennessee (1)

- How-to-Choose-the-Best-Realtor-in-Franklin--Tennessee (1)

- How-to-Choose-the-Best-Realtor-in-Hendersonville--Tennessee (1)

- How-to-Choose-the-Best-Realtor-in-Nashville---Middle-Tennessee-for-Your-Next-Move (1)

- How-to-Choose-the-Right-Nashville-Suburb-for-Your-Lifestyle (1)

- HOW-TO-CHOOSE-THE-RIGHT-REALTOR-IN-MIDDLE-TENNESSEE-IN-A-SHIFTING-BUYER-FRIENDLY-MARKET (1)

- How-to-Compete-in-Nashville-s-Hot-Housing-Market-Without-Overpaying (1)

- How-to-Find-the-Best-Deals-on-Homes-in-Nashville-Right-Now (1)

- How-to-Find-the-Right-Realtor-in-Nashville---Middle-Tennessee-When-Relocating-or-Buying-a-Home (1)

- How-to-Find-the-Right-Realtor-in-Nashville-and-Middle-Tennessee--Buyer---Seller-Guide- (1)

- How-to-Get-Pre-Approved-for-a-Home-Loan-in-Nashville (1)

- How-to-Make-a-Competitive-Offer-on-a-Nashville-Home-Without-Overpaying (1)

- How-to-Negotiate-Repairs-After-a-Home-Inspection-in-Nashville (1)

- How-to-Spot-a-Great-Deal-in-the-Nashville-Housing-Market (1)

- How-to-Win-a-Multiple-Offer-Situation-When-Buying-in-Nashville (1)

- How-to-Work-With-a-Nashville-REALTOR-to-Find-Your-Perfect-Home (1)

- Investing (1)

- Investment Properties (1)

- Is-Brentwood--TN-a-Good-Place-to-Raise-a-Family--Nashville-s-Nik-Explains-Why-Parents-Love-It (1)

- Is-Brentwood--TN-a-Good-Place-to-Raise-a-Family--Nashville-s-Nik-Shares-Why-Parents-Love-It-Here (1)

- Is-Brentwood--TN-a-Good-Place-to-Raise-Kids--Nik-Shewmaker-s-Honest-Take (1)

- Is-Brentwood--TN-a-Good-Place-to-Retire--Nashville-s-Nik-Shares-Why-It-s-Ideal-for-Active-Adults (1)

- Is-Brentwood--TN-a-Safe-Place-to-Live--Nashville-s-Nik-Breaks-Down-the-Facts (1)

- Is-Brentwood--TN-Expensive--Breaking-Down-the-Real-Cost-of-Living-with-Nashville-s-Nik (1)

- Is-Brentwood--TN-Expensive--Nashville-s-Nik-Breaks-Down-the-Cost-of-Living (1)

- Is-Brentwood--TN-Expensive--Nashville-s-Nik-Breaks-Down-the-Real-Costs-of-Living-Well (1)

- Is-Brentwood--TN-Expensive--Nashville-s-Nik-Explains-Why-It-s-Worth-Every-Penny (1)

- Is-Brentwood--TN-Safe--Nashville-s-Nik-Shares-the-Truth-About-Crime-and-Community (1)

- Is-Buying-a-Home-in-Nashville-a-Good-Investment-in-2025 (1)

- Is-It-Smarter-to-Buy-a-Home-in-Nashville-Before-Interest-Rates-Drop-Again- (1)

- Is-Nashville-a-Good-Place-to-Retire- (1)

- Is-Now-a-Good-Time-to-Buy-a-Home-in-Nashville-With-Today-s-Interest-Rates- (1)

- Is-Relocating-to-Nashville-a-Good-Idea-in-2025- (1)

- Lakefront Living (2)

- Listing Agent (1)

- Luxury Homes (3)

- Luxury Real Estate (1)

- Market Updates (1)

- Middle Tennessee Real Estate (1)

- Moving to Middle Tennessee: What Newcomers Need to Know (1)

- Moving-from-New-York-to-Tennessee--Here-s-What-You-Should-Know--From-a-Nashville-Relocation-Specialist- (1)

- Moving-to-Nashville--How-to-Choose-the-Right-Realtor-Before-You-Relocate-to-Middle-Tennessee (1)

- Nashville (1)

- Nashville Neighborhoods (1)

- Nashville Real Estate (6)

- Nashville Real Estate Market (2)

- Nashville’s Musical Roots: Museums, Hidden Gems, and a DIY Walking Tour (1)

- Neighborhood Guides (1)

- New Construction (2)

- Pet-Friendly Spots in Middle Tennessee: Parks, Patios, and More (1)

- Real Estate Advice (1)

- Real Estate Tips (1)

- Relocating to Nashville From Out of State? Here’s How to Do It Right (1)

- Relocation Guide (1)

- Relocation to Nashville (1)

- Seasonal Home Maintenance Tips for Middle Tennessee Homeowners (2)

- Seller Resources (13)

- Selling Your Home (1)

- Selling Your Home Without an Agent in Nashville, TN: What to Know (1)

- Should I Sell My Home Before or After Buying a New One in Nashville, TN? (1)

- Should I Sell My Home Now or Wait in Nashville, TN? (1)

- Should I Sell My Home or Rent It Out in Nashville, TN? (1)

- Should I Stage My Home Before Selling in Nashville, TN? (1)

- Should I Stage My Nashville Home Before I Sell It? (1)

- Should You Sell Your Home Before Buying a New One in Nashville, TN? (1)

- Should-I-Rent-or-Buy-a-Home-in-Nashville-Right-Now----Expert-Advice-From-Nik-Shewmaker-REALTOR (1)

- Should-I-Use-a-Local-Nashville-Lender-or-a-Big-Bank-to-Buy-My-Home- (1)

- The Best Places to Live in Middle Tennessee for Familie (1)

- The Titans of Nashville: Exploring the Largest Companies Shaping Music City (1)

- The-Ultimate-Nashville-Home-Buyer-s-Checklist-for-2025 (2)

- Things I Love About Providence Marketplace in Mount Juliet (1)

- Top 3 State Parks in Middle Ten (1)

- Top 5 Can’t-Miss Family-Friendly Festivals in Nashville, Tennessee – June 2025 (1)

- Top Lakes in Middle Tennessee for Boating, Fishing, and Swimming Nik S (1)

- Top Things to Do in Mount Juliet, Tennessee: A Local’s Guide to Fun and Adventure (1)

- Top Upscale Restaurants in Brentwood, Tennessee (1)

- Understanding-Closing-Costs-When-Buying-a-Home-in-Nashville (1)

- What Are the Most Common Mistakes When Selling a Home in Nashville, TN? (1)

- What Are the Pros and Cons of Selling a Home Without a Realtor in Nashville, TN? (1)

- What Happens After I Accept an Offer on My Home in Nashville? (1)

- What Happens After You Accept an Offer on Your Home in Nashville, TN? (1)

- What Happens After You Sell Your Home in Nashville, TN? (1)

- What Happens at a Home Appraisal in Nashville, TN? (1)

- What Is the Average Time to Sell a Home in Nashville, TN? (1)

- What Is the First Step in Selling Your Home in Nashville, TN? (1)

- What Paperwork Do I Need to Sell My Home in Nashville? (1)

- What to Do Before You Sell Your Home in Nashville, TN (2)

- What to Expect When Selling Your Home in Nashville’s Current Market (1)

- What to Expect When You Sell Your Home in Nashville, TN (1)

- What to Fix Before Selling a Home in Nashville, TN (1)

- What-Are-Closing-Costs-When-Buying-a-Home-in-Nashville--TN- (1)

- What-Are-the-Best-First-Time-Buyer-Loan-Programs-in-Tennessee- (1)

- What-Are-the-Best-Neighborhoods-in-Brentwood--TN--Nashville-s-Nik-Shares-Her-Local-Favorites (1)

- What-Are-the-Best-Neighborhoods-in-Brentwood--TN-for-Families--A-Local-s-Guide-by-Nik-Shewmaker (1)

- What-Are-the-Hidden-Costs-of-Buying-a-Home-in-Nashville- (1)

- What-Are-the-Hidden-Costs-of-Relocating-to-Nashville- (1)

- What-Are-the-Pros-and-Cons-of-Moving-to-Nashville-in-2025- (1)

- What-Are-the-Pros-and-Cons-of-Relocating-to-Nashville-in-2025- (1)

- What-Are-the-Safest-Neighborhoods-in-Nashville-for-New-Residents- (1)

- What-Credit-Score-Do-You-Need-to-Buy-a-Home-in-Nashville--TN- (1)

- What-Do-I-Need-to-Know-Before-Moving-to-Nashville (1)

- What-Do-I-Need-to-Know-Before-Moving-to-Nashville- (1)

- What-I-Wish-I-Knew-Before-Buying-My-First-Home-in-Nashville (3)

- What-Is-the-Average-Commute-From-Brentwood--TN-to-Downtown-Nashville--Real-Insight-from-Nik-Shewmaker (1)

- What-Is-the-Average-Home-Price-in-Brentwood--TN--Nashville-s-Nik-Breaks-Down-the-Market (1)

- What-Is-the-Average-Mortgage-Payment-for-a-Home-in-Nashville-in-2025- (1)

- What-Is-the-Easiest-Way-to-Buy-a-House (1)

- What-Is-the-Easiest-Way-to-Buy-a-House-in-Nashville-in-Today-s-Market- (1)

- What-Jobs-Are-Bringing-People-to-Nashville- (1)

- What-s-It-Like-Living-in-Brentwood--TN--Nashville-s-Nik-Shares-a-Local-s-Honest-Take (1)

- What-s-It-Like-Living-in-Brentwood--TN--Nashville-s-Nik-Shares-a-Local-s-Perspective (1)

- What-s-the-Best-Time-of-Year-to-Relocate-to-Nashville- (1)

- What-s-the-Cost-of-Living-in-Nashville-Compared-to-Other-Cities- (1)

- What-s-the-Weather-Like-in-Brentwood--TN--Nashville-s-Nik-Shares-What-to-Expect-Year-Round (1)

- What-Should-I-Know-About-Nashville-s-Weather-Before-Relocating- (1)

- What-to-Know-About-Homeowners-Insurance-When-Buying-in-Nashville (1)

- What’s the Best Time of Year to Sell a Home in Nashville, TN? (1)

- When to Sell Your Home in Franklin, TN (1)

- Where-Are-the-Best-Neighborhoods-in-Nashville-for-Relocating-Families- (1)

- Why Are Homes in Nashville Not Selling Like They Used To? (1)

- Why-Are-So-Many-People-Moving-to-Brentwood--TN--Nashville-s-Nik-Explains-the-Hype (1)

- Why-Are-So-Many-People-Moving-to-Brentwood--TN--Nashville-s-Nik-Explains-the-Surge (1)

- Why-So-Many-New-Yorkers-Are-Moving-to-Tennessee (1)

- Why-Waiting-to-Buy-a-Home-in-Nashville-Could-Cost-You-More (1)

- Why-Working-With-a-Local-Expert-Like-Nik-Shewmaker-REALTOR-Can-Save-You-Thousands (1)

- Why-You-Shouldn-t-Skip-the-Home-Inspection-When-Buying-in-Nashville (1)

Recent Posts